[ad_1]

When the Fed raises rates of interest, how does inflation reply? Are there “lengthy and variable lags” to inflation and output?

There’s a normal story: The Fed raises rates of interest; inflation is sticky so actual rates of interest (rate of interest – inflation) rise; increased actual rates of interest decrease output and employment; the softer financial system pushes inflation down. Every of those is a lagged impact. However regardless of 40 years of effort, concept struggles to substantiate that story (subsequent put up), it is needed to see within the information (final put up), and the empirical work is ephemeral — this put up.

The vector autoregression and associated native projection are at this time the usual empirical instruments to deal with how financial coverage impacts the financial system, and have been since Chris Sims’ nice work within the Seventies. (See Larry Christiano’s evaluate.)

I’m shedding religion within the methodology and outcomes. We have to discover new methods to study concerning the results of financial coverage. This put up expands on some ideas on this matter in “Expectations and the Neutrality of Curiosity Charges,” a number of of my papers from the Nineteen Nineties* and wonderful current evaluations from Valerie Ramey and Emi Nakamura and Jón Steinsson, who eloquently summarize the laborious identification and computation troubles of up to date empirical work.

Perhaps in style knowledge is correct, and economics simply has to catch up. Maybe we’ll. However a preferred perception that doesn’t have stable scientific concept and empirical backing, regardless of a 40 yr effort for fashions and information that may present the specified reply, have to be a bit much less reliable than one which does have such foundations. Sensible folks ought to think about that the Fed could also be much less highly effective than historically thought, and that its rate of interest coverage has completely different results than generally thought. Whether or not and underneath what situations excessive rates of interest decrease inflation, whether or not they accomplish that with lengthy and variable however nonetheless predictable and exploitable lags, is way much less sure than you suppose.

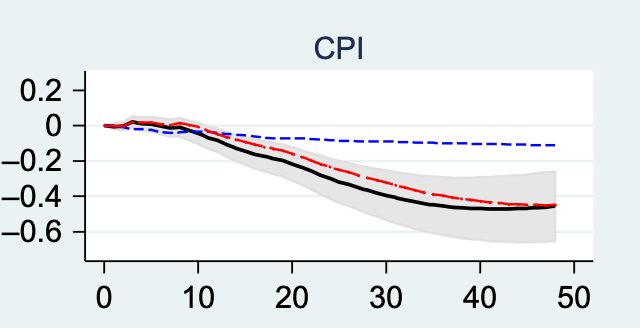

The black traces plot the unique specification. The highest left panel plots the trail of the Federal Funds fee after the Fed unexpectedly raises the rate of interest. The funds fee goes up, however just for 6 months or so. Industrial manufacturing goes down and unemployment goes up, peaking at month 20. The determine plots the degree of the CPI, so inflation is the slope of the decrease proper hand panel. You see inflation goes the “mistaken” method, up, for about 6 months, after which gently declines. Rates of interest certainly appear to have an effect on the financial system with lengthy lags.

This was the broad define of consensus empirical estimates for a few years. It is not uncommon to many different research, and it’s according to the beliefs of coverage makers and analysts. It is just about what Friedman (1968) informed us to anticipate. Getting modern fashions to supply one thing like that is a lot tougher, however that is the subsequent weblog put up.

I attempt to preserve this weblog accessible to nonspecialists, so I am going to step again momentarily to elucidate how we produce graphs like these. Economists who know what a VAR is ought to skip to the subsequent part heading.

How can we measure the impact of financial coverage on different variables? Milton Friedman and Anna Schwartz kicked it off within the Financial Historical past by pointing to the historic correlation of cash development with inflation and output. They knew as we do this correlation is just not causation, so that they pointed to the truth that cash development preceeded inflation and output development. However as James Tobin identified, the cock’s crow comes earlier than, however doesn’t trigger, the solar to rise. So too folks might go get out some cash forward of time after they see extra future enterprise exercise on the horizon. Even correlation with a lead is just not causation. What to do? Clive Granger’s causality and Chris Sims’ VAR, particularly “Macroeconomics and Actuality” gave at this time’s reply. (And there’s a purpose that everyone talked about to date has a Nobel prize.)

First, we discover a financial coverage “shock,” a motion within the rate of interest (as of late; cash, then) that’s plausibly not a response to financial occasions and particularly to anticipated future financial occasions. We consider the Fed setting rates of interest by a response to financial information plus deviations from that response, akin to

rate of interest = (#) output + (#) inflation + (#) different variables + disturbance.

We wish to isolate the “disturbance,” actions within the rate of interest not taken in response to financial occasions. (I exploit “shock” to imply an unpredictable variable, and “disturbance” to imply deviation from an equation just like the above, however one that may persist for some time. A financial coverage “shock” is an surprising motion within the disturbance.) The “rule” half right here will be however needn’t be the Taylor rule, and might embody different variables than output and inflation. It’s what the Fed normally does given different variables, and subsequently (hopefully) controls for reverse causality from anticipated future financial occasions to rates of interest.

Now, in any particular person episode, output and inflation and inflation following a shock might be influenced by subsequent shocks to the financial system, financial and different. However these common out. So, the common worth of inflation, output, employment, and so on. following a financial coverage shock is a measure of how the shock impacts the financial system all by itself. That’s what has been plotted above.

VARs had been one of many first massive advances within the trendy empirical quest to seek out “exogenous” variation and (considerably) credibly discover causal relationships.

Largely the large literature varies on how one finds the “shocks.” Conventional VARs use regressions of the above equations and the residual is the shock, with an enormous query simply what number of and which contemporaneous variables one provides within the regression. Romer and Romer pioneered the “narrative method,” studying the Fed minutes to isolate shocks. Some technical particulars on the backside and rather more dialogue beneath. The bottom line is discovering shocks. One can simply regress output and inflation on the shocks to supply the response operate, which is a “native projection” not a “VAR,” however I am going to use “VAR” for each strategies for lack of a greater encompassing phrase.

What’s a “shock” anyway? The idea is that the Fed considers its forecast of inflation, output and different variables it’s making an attempt to manage, gauges the same old and acceptable response, after which provides 25 or 50 foundation factors, at random, only for the heck of it. The query VARS attempt to reply is similar: What occurs to the financial system if the Fed raises rates of interest unexpectedly, for no explicit purpose in any respect?

However the Fed by no means does this. Ask them. Learn the minutes. The Fed doesn’t roll cube. They at all times elevate or decrease rates of interest for a purpose, that purpose is at all times a response to one thing happening within the financial system, and more often than not the way it impacts forecasts of inflation and employment. There aren’t any shocks as outlined.

I speculated right here that we would get round this drawback: If we knew the Fed was responding to one thing that had no correlation with future output, then although that’s an endogenous response, then it’s a legitimate motion for estimating the impact of rates of interest on output. My instance was, what if the Fed “responds” to the climate. Nicely, although endogenous, it is nonetheless legitimate for estimating the impact on output.

The Fed does reply to numerous issues, together with overseas trade, monetary stability points, fairness, terrorist assaults, and so forth. However I can not consider any of those during which the Fed is just not pondering of those occasions for his or her impact on output and inflation, which is why I by no means took the concept far. Perhaps you may.

Shock isolation additionally relies on full controls for the Fed’s info. If the Fed makes use of any details about future output and inflation that’s not captured in our regression, then details about future output and inflation stays within the “shock” collection.

The well-known “value puzzle” is an effective instance. For the primary few a long time of VARs, rate of interest shocks appeared to result in increased inflation. It took an extended specification search to do away with this undesired end result. The story was, that the Fed noticed inflation coming in methods not utterly managed for by the regression. The Fed raised rates of interest to attempt to forestall the inflation, however was a bit hesitant about it so didn’t remedy the inflation that was coming. We see increased rates of interest adopted by increased inflation, although the true causal impact of rates of interest goes the opposite method. This drawback was “cured” by including commodity costs to the rate of interest rule, on the concept fast-moving commodity costs would seize the knowledge the Fed was utilizing to forecast inflation. (Apparently as of late we appear to see core inflation as one of the best forecaster, and throw out commodity costs!) With these and a few cautious orthogonalization decisions, the “value puzzle” was tamped right down to the one yr or so delay you see above. (Neo-Fisherians may object that perhaps the worth puzzle was making an attempt to inform us one thing all these years!)

Nakamura and Steinsson write of this drawback:

“What’s being assumed is that controlling for a couple of lags of some variables captures all endogenous variation in coverage… This appears extremely unlikely to be true in follow. The Fed bases its coverage selections on an enormous quantity of information. Totally different concerns (in some instances extremely idiosyncratic) have an effect on coverage at completely different occasions. These embody stress within the banking system, sharp modifications in commodity costs, a current inventory market crash, a monetary disaster in rising markets, terrorist assaults, short-term funding tax credit, and the Y2K laptop glitch. The checklist goes on and on. Every of those concerns might solely have an effect on coverage in a significant method on a small variety of dates, and the variety of such influences is so massive that it’s not possible to incorporate all of them in a regression. However leaving any certainly one of them out will end in a financial coverage “shock” that the researcher views as exogenous however is in actual fact endogenous.”

Nakamura and Steinsson supply 9/11 as one other instance summarizing my “excessive frequency identification” paper with Monika Piazzesi: The Fed lowered rates of interest after the terrorist assault, possible reacting to its penalties for output and inflation. However VARs register the occasion as an exogenous shock.

Romer and Romer instructed that we use Fed Greenbook forecasts of inflation and output as controls, as these ought to characterize the Fed’s full info set. They supply narrative proof that Fed members belief Buck forecasts greater than you may suspect.

This situation is a common Achilles heel of empirical macro and finance: Does your process assume brokers see no extra info than you will have included within the mannequin or estimate? If sure, you will have an issue. Equally, “Granger causality” solutions the cock’s crow-sunrise drawback by saying that if surprising x leads surprising y then x causes y. Nevertheless it’s solely actual causality if the “anticipated” consists of all info, as the worth puzzle counterexample exhibits.

Simply what properties do we want of a shock in an effort to measure the response to the query, “what if the Fed raised charges for no purpose?” This strikes me as a little bit of an unsolved query — or somewhat, one that everybody thinks is so apparent that we do not actually take a look at it. My suggestion that the shock solely want be orthogonal to the variable whose response we’re estimating is casual, and I do not know of formal literature that is picked it up.

Should “shocks” be surprising, i.e. not forecastable from something within the earlier time info set? Should they shock folks? I do not suppose so — it’s neither mandatory nor ample for shock to be unforecastable for it to establish the inflation and output responses. Not responding to anticipated values of the variable whose response you wish to measure ought to be sufficient. If bond markets discovered a few random funds fee rise in the future forward, it could then be an “anticipated” shock, however clearly simply pretty much as good for macro. Romer and Romer have been criticized that their shocks are predictable, however this will likely not matter.

The above Nakamura and Steinsson quote says leaving out any info results in a shock that’s not strictly exogenous. However strictly exogenous is probably not mandatory for estimating, say, the impact of rates of interest on inflation. It is sufficient to rule out reverse causality and third results.

Both I am lacking a well-known econometric literature, as is everybody else writing the VARs I’ve learn who do not cite it, or there’s a good concept paper to be written.

Romer and Romer, pondering deeply about the way to learn “shocks” from the Fed minutes, outline shocks thus to avoid the “there aren’t any shocks” drawback:

we search for occasions when financial policymakers felt the financial system was roughly at potential (or regular) output, however determined that the prevailing fee of inflation was too excessive. Policymakers then selected to chop cash development and lift rates of interest, realizing that there could be (or at the least may very well be) substantial detrimental penalties for combination output and unemployment. These standards are designed to pick occasions when policymakers basically modified their tastes concerning the acceptable degree of inflation. They weren’t simply responding to anticipated actions in the true financial system and inflation.

[My emphasis.] You possibly can see the problem. This isn’t an “exogenous” motion within the funds fee. It’s a response to inflation, and to anticipated inflation, with a transparent eye on anticipated output as effectively. It truly is a nonlinear rule, ignore inflation for some time till it will get actually unhealthy then lastly get severe about it. Or, as they are saying, it’s a change in rule, a rise within the sensitivity of the brief run rate of interest response to inflation, taken in response to inflation seeming to get uncontrolled in an extended run sense. Does this establish the response to an “exogenous” rate of interest improve? Probably not. However perhaps it would not matter.

- Are we even asking an attention-grabbing query?

The entire query, what would occur if the Fed raised rates of interest for no purpose, is arguably in addition to the purpose. At a minimal, we ought to be clearer about what query we’re asking, and whether or not the insurance policies we analyze are implementations of that query.

The query presumes a secure “rule,” (e.g. (i_t = rho i_{t-1} phi_pi pi_t + phi_x x_t + u_t)) and asks what occurs in response to a deviation ( +u_t ) from the rule. Is that an attention-grabbing query? The usual story for 1980-1982 is strictly not such an occasion. Inflation was not conquered by an enormous “shock,” an enormous deviation from Seventies follow, whereas protecting that follow intact. Inflation was conquered (so the story goes) by a change within the rule, by an enormous improve in $phi_pi$. That change raised rates of interest, however arguably with none deviation from the brand new rule (u_t) in any respect. Considering when it comes to the Phillips curve ( pi_t = E_t pi_{t+1} + kappa x_t), it was not an enormous detrimental (x_t) that introduced down inflation, however the credibility of the brand new rule that introduced down (E_t pi_{t+1}).

If the artwork of lowering inflation is to persuade folks {that a} new regime has arrived, then the response to any financial coverage “shock” orthogonal to a secure “rule” utterly misses that coverage.

Romer and Romer are nearly speaking a few rule-change occasion. For 2022, they is likely to be trying on the Fed’s abandonment of versatile common inflation focusing on and its return to a Taylor rule. Nevertheless, they do not acknowledge the significance of the excellence, treating modifications in rule as equal to a residual. Altering the rule modifications expectations in fairly other ways from a residual of a secure rule. Modifications with an even bigger dedication ought to have larger results, and one ought to standardize by some means by the dimensions and permanence of the rule change, not essentially the dimensions of the rate of interest rise. And, having requested “what if the Fed modifications rule to be extra severe about inflation,” we actually can not use the evaluation to estimate what occurs if the Fed shocks rates of interest and doesn’t change the rule. It takes some mighty invariance end result from an financial concept {that a} change in rule has the identical impact as a shock to a given rule.

There isn’t any proper and mistaken, actually. We simply must be extra cautious about what query the empirical process asks, if we wish to ask that query, and if our coverage evaluation truly asks the identical query.

- Estimating guidelines, Clarida Galí and Gertler.

Clarida, Galí, and Gertler (2000) is a justly well-known paper, and on this context for doing one thing completely completely different to guage financial coverage. They estimate guidelines, fancy variations of (i_t = rho i_{t-1} phi_pi pi_t + phi_x x_t + u_t), they usually estimate how the (phi) parameters change over time. They attribute the tip of Seventies inflation to a change within the rule, an increase in (phi_pi) from the Seventies to the Eighties. Of their mannequin, the next ( phi_pi) leads to much less risky inflation. They don’t estimate any response capabilities. The remainder of us had been watching the mistaken factor all alongside. Responses to shocks weren’t the attention-grabbing amount. Modifications within the rule had been the attention-grabbing amount.

Sure, I criticized the paper, however for points which are irrelevant right here. (Within the new Keynesian mannequin, the parameter that reduces inflation is not the one they estimate.) The essential level right here is that they’re doing one thing utterly completely different, and supply us a roadmap for the way else we would consider financial coverage if not by impulse-response capabilities to financial coverage shocks.

The attention-grabbing query for fiscal concept is, “What’s the impact of an rate of interest rise not accompanied by a change in fiscal coverage?” What can the Fed do by itself?

Against this, normal fashions (each new and outdated Keynesian) embody concurrent fiscal coverage modifications when rates of interest rise. Governments tighten in current worth phrases, at the least to pay increased curiosity prices on the debt and the windfall to bondholders that flows from surprising disinflation.

Expertise and estimates certainly embody fiscal modifications together with financial tightening. Each fiscal and financial authorities react to inflation with coverage actions and reforms. Development-oriented microeconomic reforms with fiscal penalties typically observe as effectively — rampant inflation might have had one thing to do with Carter period trucking, airline, and telecommunications reform.

But no present estimate tries to search for a financial shock orthogonal to fiscal coverage change. The estimates we now have are at finest the results of financial coverage along with no matter induced or coincident fiscal and microeconomic coverage tends to occur similtaneously central banks get severe about combating inflation. Figuring out the part of a financial coverage shock orthogonal to fiscal coverage, and measuring its results is a primary order query for fiscal concept of financial coverage. That is why I wrote this weblog put up. I got down to do it, after which began to confront how VARs are already falling aside in our fingers.

Simply what “no change in fiscal coverage” means is a vital query that varies by software. (Tons extra in “fiscal roots” right here, fiscal concept of financial coverage right here and in FTPL.) For easy calculations, I simply ask what occurs if rates of interest change with no change in major surplus. One may additionally outline “no change” as no change in tax charges, automated stabilizers, and even routine discretionary stimulus and bailout, no disturbance (u_t) in a fiscal rule (s_t = a + theta_pi pi_t + theta_x x_t + … + u_t). There isn’t any proper and mistaken right here both, there may be simply ensuring you ask an attention-grabbing query.

- Lengthy and variable lags, and chronic rate of interest actions

The primary plot exhibits a mighty lengthy lag between the monitor coverage shock and its impact on inflation and output. That does not imply that the financial system has lengthy and variable lags.

This plot is definitely not consultant, as a result of within the black traces the rate of interest itself rapidly reverts to zero. It is not uncommon to discover a extra protracted rate of interest response to the shock, as proven within the pink and blue traces. That mirrors widespread sense: When the Fed begins tightening, it units off a yr or so of stair-step additional will increase, after which a plateau, earlier than comparable stair-step reversion.

That raises the query, does the long-delayed response of output and inflation characterize a delayed response to the preliminary financial coverage shock, or does it characterize an almost instantaneous response to the upper subsequent rates of interest that the shock units off?

One other method of placing the query, is the response of inflation and output invariant to modifications within the response of the funds fee itself? Do persistent and transitory funds fee modifications have the identical responses? For those who consider the inflation and output responses as financial responses to the preliminary shock solely, then it doesn’t matter if rates of interest revert instantly to zero, or go on a ten yr binge following the preliminary shock. That looks as if a reasonably sturdy assumption. For those who suppose {that a} extra persistent rate of interest response would result in a bigger or extra persistent output and inflation response, you then suppose a few of what we see within the VARs is a fast structural response to the later increased rates of interest, after they come.

Again in 1988, I posed this query in “what do the VARs imply?” and confirmed you may learn it both method. The persistent output and inflation response can characterize both lengthy financial lags to the preliminary shock, or a lot much less laggy responses to rates of interest after they come. I confirmed the way to deconvolute the response operate to the structural impact of rates of interest on inflation and output and the way persistently rates of interest rise. The inflation and output responses is likely to be the identical with shorter funds fee responses, or they is likely to be a lot completely different.

Clearly (although typically forgotten), whether or not the inflation and output responses are invariant to modifications within the funds fee response wants a mannequin. If within the financial mannequin solely surprising rate of interest actions have an effect on output and inflation, although with lags, then the responses are as conventionally learn structural responses and invariant to the rate of interest path. There isn’t any such financial mannequin. Lucas (1972) says solely surprising cash impacts output, however with no lags, and anticipated cash impacts inflation. New Keynesian fashions have very completely different responses to everlasting vs. transitory rate of interest shocks.

Apparently, Romer and Romer don’t see it this fashion, and regard their responses as structural lengthy and variable lags, invariant to the rate of interest response. They opine that given their studying of a constructive shock in 2022, an extended and variable lag to inflation discount is baked in, it doesn’t matter what the Fed does subsequent. They argue that the Fed ought to cease elevating rates of interest. (In equity, it would not appear like they thought concerning the situation a lot, so that is an implicit somewhat than specific assumption.) The choice view is that results of a shock on inflation are actually results of the following fee rises on inflation, that the impulse response operate to inflation is just not invariant to the funds fee response, so stopping the usual tightening cycle would undo the inflation response. Argue both method, however at the least acknowledge the essential assumption behind the conclusions.

Was the success of inflation discount within the early Eighties only a lengthy delayed response to the primary few shocks? Or was the early Eighties the results of persistent massive actual rates of interest following the preliminary shock? (Or, one thing else totally, a coordinated fiscal-monetary reform… However I am staying away from that and simply discussing standard narratives, not essentially the suitable reply.) If the latter, which is the standard narrative, you then suppose it does matter if the funds fee shock is adopted by extra funds fee rises (or constructive deviations from a rule), that the output and inflation response capabilities don’t instantly measure lengthy lags from the preliminary shock. De-convoluting the structural funds fee to inflation response and the persistent funds fee response, you’d estimate a lot shorter structural lags.

Nakamura and Steinsson are of this view:

Whereas the Volcker episode is according to a considerable amount of financial nonneutrality, it appears much less according to the generally held view that financial coverage impacts output with “lengthy and variable lags.” On the contrary, what makes the Volcker episode probably compelling is that output fell and rose largely in sync with the actions [interest rates, not shocks] of the Fed.

And that is a superb factor too. We have accomplished lots of dynamic economics since Friedman’s 1968 tackle. There may be actually nothing in dynamic financial concept that produces a structural long-delayed response to shocks, with out the continued strain of excessive rates of interest.

Nevertheless, if the output and inflation responses are not invariant to the rate of interest response, then the VAR instantly measures an extremely slender experiment: What occurs in response to a shock rate of interest rise, adopted by the plotted path of rates of interest? And that plotted path is normally fairly short-term, as within the above graph. What would occur if the Fed raised charges and saved them up, a la 1980? The VAR is silent on that query. It’s good to calibrate some mannequin to the responses we now have to deduce that reply.

VARs and shock responses are sometimes misinterpret as generic theory-free estimates of “the results of financial coverage.” They aren’t. At finest, they inform you the impact of 1 particular experiment: A random improve in funds fee, on high of a secure rule, adopted by the same old following path of funds fee. Any different implication requires a mannequin, specific or implicit.

Extra particularly, with out that clearly false invariance assumption, VARs can not instantly reply a bunch of essential questions. Two on my thoughts: 1) What occurs if the Fed raises rates of interest completely? Does inflation finally rise? Does it rise within the brief run? That is the “Fisherian” and “neo-Fisherian” questions, and the reply “sure” pops unexpectedly out of the usual new-Keynesian mannequin. 2) Is the short-run detrimental response of inflation to rates of interest stronger for extra persistent fee rises? The long-term debt fiscal concept mechanism for a short-term inflation decline is tied to the persistence of the shock and the maturity construction of the debt. The responses to short-lived rate of interest actions (high left panel) are silent on these questions.

Immediately is a vital qualifier. It’s not unattainable to reply these questions, however it’s important to work tougher to establish persistent rate of interest shocks. For instance, Martín Uribe identifies everlasting vs. transitory rate of interest shocks, and finds a constructive response of inflation to everlasting rate of interest rises. How? You possibly can’t simply select the rate of interest rises that turned out to be everlasting. It’s important to discover shocks or elements of the shock which are ex-ante predictably going to be everlasting, based mostly on different forecasting variables and the correlation of the shock with different shocks. For instance, a short-term fee shock that additionally strikes long-term charges is likely to be extra everlasting than one which doesn’t accomplish that. (That requires the expectations speculation, which does not work, and long run rates of interest transfer an excessive amount of anyway in response to transitory funds fee shocks. So, this isn’t instantly a suggestion, simply an instance of the sort of factor one should do. Uribe’s mannequin is extra advanced than I can summarize in a weblog.) Given how small and ephemeral the shocks are already, subdividing them into these which are anticipated to have everlasting vs. transitory results on the federal funds fee is clearly a problem. Nevertheless it’s not unattainable.

- Financial coverage shocks account for small fractions of inflation, output and funds fee variation.

Friedman thought that almost all recessions and inflations had been resulting from financial errors. The VARs fairly uniformly deny that end result. The consequences of financial coverage shocks on output and inflation add as much as lower than 10 p.c of the variation of output and inflation. Partially the shocks are small, and partly the responses to the shocks are small. Most recessions come from different shocks, not financial errors.

Worse, each in information and in fashions, most inflation variation comes from inflation shocks, most output variation comes from output shocks, and so on. The cross-effects of 1 variable on one other are small. And “inflation shock” (or “marginal price shock”), “output shock” and so forth are simply labels for our ignorance — error phrases in regressions, unforecasted actions — not independently measured portions.

(This and outdated level, for instance in my 1994 paper with the nice title “Shocks.” Technically, the variance of output is the sum of the squares of the impulse-response capabilities — the plots — occasions the variance of the shocks. Thus small shocks and small responses imply not a lot variance defined.)

This can be a deep level. The beautiful consideration put to the results of financial coverage in new-Keynesian fashions, whereas attention-grabbing to the Fed, are then largely irrelevant in case your query is what causes recessions. Complete fashions work laborious to match all the responses, not simply to financial coverage shocks. Nevertheless it’s not clear that the nominal rigidities which are essential for the results of financial coverage are deeply essential to different (provide) shocks, and vice versa.

This isn’t a criticism. Economics at all times works higher if we will use small fashions that concentrate on one factor — development, recessions, distorting impact of taxes, impact of financial coverage — with out having to have a mannequin of the whole lot during which all results work together. However, be clear we now not have a mannequin of the whole lot. “Explaining recessions” and “understanding the results of financial coverage” are considerably separate questions.

Financial coverage shocks additionally account for small fractions of the motion within the federal funds fee itself. Many of the funds fee motion is within the rule, the response to the financial system time period. Like a lot empirical economics, the hunt for causal identification leads us to have a look at a tiny causes with tiny results, that do little to elucidate a lot variation within the variable of curiosity (inflation). Nicely, trigger is trigger, and the needle is the sharpest merchandise within the haystack. However one worries concerning the robustness of such tiny results, and to what extent they summarize historic expertise.

To be concrete, here’s a typical shock regression, 1960:1-2023:6 month-to-month information, normal errors in parentheses:

ff(t) = a + b ff(t-1) + c[ff(t-1)-ff(t-2)] + d CPI(t) + e unemployment(t) + financial coverage shock,

| ff(t-1) | ff(t-1)-ff(t-2) | CPI | Unemp | R2 |

|---|---|---|---|---|

| 0.97 | 0.39 | 0.032 | -0.017 | 0.985 |

| (0.009) | (0.07) | (0.013) | (0.009) |

The funds fee is persistent — the lag time period (0.97) is massive. Current modifications matter too: As soon as the Fed begins a tightening cycle, it is prone to preserve elevating charges. And the Fed responds to CPI and unemployment.

The plot exhibits the precise federal funds fee (blue), the mannequin or predicted federal funds fee (pink), the shock which is the distinction between the 2 (orange) and the Romer and Romer dates (vertical traces). You possibly can’t see the distinction between precise and predicted funds fee, which is the purpose. They’re very comparable and the shocks are small. They’re nearer horizontally than vertically, so the vertical distinction plotted as shock remains to be seen.

The shocks are a lot smaller than the funds fee, and smaller than the rise and fall within the funds fee in a typical tightening or loosening cycle. The shocks are bunched, with by far the most important ones within the early Eighties. The shocks have been tiny for the reason that Eighties. (Romer and Romer do not discover any shocks!)

Now, our estimates of the impact of financial coverage take a look at the typical values of inflation, output, and employment within the 4-5 years after a shock. Actually, you say, trying on the graph? That is going to be dominated by the expertise of the early Eighties. And with so many constructive and detrimental shocks shut collectively, the typical worth 4 years later goes to be pushed by delicate timing of when the constructive or detrimental shocks line up with later occasions.

Put one other method, here’s a plot of inflation 30 months after a shock regressed on the shock. Shock on the x axis, subsequent inflation on the y axis. The slope of the road is our estimate of the impact of the shock on inflation 30 months out (supply, with particulars). Hmm.

Yet another graph (I am having enjoyable right here):

This can be a plot of inflation for the 4 years after every shock, occasions that shock. The correct hand aspect is similar graph with an expanded y scale. The common of those histories is our impulse response operate. (The large traces are the episodes which multiply the massive shocks of the early Eighties. They principally converge as a result of, both multiplied by constructive or detrimental shocks, inflation wend down within the Eighties.)

Impulse response capabilities are simply quantitative summaries of the teachings of historical past. You might be underwhelmed that historical past is sending a transparent story.

Once more, welcome to causal economics — tiny common responses to tiny however recognized actions is what we estimate, not broad classes of historical past. We don’t estimate “what’s the impact of the sustained excessive actual rates of interest of the early Eighties,” for instance, or “what accounts for the sharp decline of inflation within the early Eighties?” Maybe we must always, although confronting endogeneity of the rate of interest responses another method. That is my predominant level at this time.

- Estimates disappear after 1982

Ramey’s first variation within the first plot is to make use of information from 1983 to 2007. Her second variation is to additionally omit the financial variables. Christiano Eichenbaum and Evans had been nonetheless pondering when it comes to cash provide management, however our Fed doesn’t management cash provide.

The proof that increased rates of interest decrease inflation disappears after 1983, with or with out cash. This too is a typical discovering. It is likely to be as a result of there merely are not any financial coverage shocks. Nonetheless, we’re driving a automobile with a yellowed AAA highway map dated 1982 on it.

Financial coverage shocks nonetheless appear to have an effect on output and employment, simply not inflation. That poses a deeper drawback. If there simply are not any financial coverage shocks, we might simply get massive normal errors on the whole lot. That solely inflation disappears factors to the vanishing Phillips curve, which would be the weak level within the concept to return. It’s the Phillips curve by which decrease output and employment push down inflation. However with out the Phillips curve, the entire normal story for rates of interest to have an effect on inflation goes away.

- Computing long-run responses

The lengthy lags of the above plot are already fairly lengthy horizons, with attention-grabbing economics nonetheless happening at 48 months. As we get involved in future neutrality, identification through future signal restrictions (financial coverage shouldn’t completely have an effect on output), and the impact of persistent rate of interest shocks, we’re involved in even longer run responses. The “future dangers” literature in asset pricing is equally crucially involved in future properties. Intuitively, we must always know this might be troublesome. There aren’t all that many nonoverlapping 4 yr intervals after rate of interest shocks to measure results, not to mention 10 yr intervals.

VARs estimate future responses with a parametric construction. Set up the information (output, inflation, rate of interest, and so on) right into a vector (x_t = [y_t ; pi_t ; i_t ; …]’), then the VAR will be written (x_{t+1} = Ax_t + u_t). We begin from zero, transfer (x_1 = u_1) in an attention-grabbing method, after which the response operate simply simulates ahead, with (x_j = A^j x_1).

However right here an oft-forgotten lesson of Eighties econometrics pops up: It’s harmful to estimate long-run dynamics by becoming a brief run mannequin after which discovering its long-run implications. Elevating matrices to the forty eighth energy (A^{48}) can do bizarre issues, the a hundred and twentieth energy (10 years) weirder issues. OLS and most probability prize one step forward (R^2), and can fortunately settle for small one step forward mis specs that add as much as massive misspecification 10 years out. (I realized this lesson within the “Random stroll in GNP.”)

Long term implications are pushed by the utmost eigenvalue of the (A) transition matrix, and its related eigenvector. (A^j = Q Lambda^j Q^{-1}). This can be a profit and a hazard. Specify and estimate the dynamics of the mix of variables with the most important eigenvector proper, and many particulars will be mistaken. However normal estimates aren’t making an attempt laborious to get these proper.

The “native projection” various instantly estimates future responses: Run regressions of inflation in 10 years on the shock at this time. You possibly can see the tradeoff: there aren’t many non-overlapping 10 yr intervals, so this might be imprecisely estimated. The VAR makes a robust parametric assumption about long-run dynamics. When it is proper, you get higher estimates. When it is mistaken, you get misspecification.

My expertise working numerous VARs is that month-to-month VARs raised to massive powers typically give unreliable responses. Run at the least a one-year VAR earlier than you begin taking a look at future responses. Cointegrating vectors are probably the most dependable variables to incorporate. They’re usually the state variable that almost all reliably carries lengthy – run responses. However take note of getting them proper. Imposing integrating and cointegrating construction by simply taking a look at items is a good suggestion.

The regression of long-run returns on dividend yields is an effective instance. The dividend yield is a cointegrating vector, and is the slow-moving state variable. A one interval VAR [left[ begin{array}{c} r_{t+1} dp_{t+1} end{array} right] = left[ begin{array}{cc} 0 & b_r 0 & rho end{array}right] + left[ begin{array}{c} r_{t} dp_{t} end{array}right]+ varepsilon_{t+1}], implies an extended horizon regression (r_{t+j} = b_r rho^j dp_{t} +) error. Direct regressions (“native projections”) (r_{t+j} = b_{r,j} dp_t + ) error give about the identical solutions, although the downward bias in (rho) estimates is a little bit of a difficulty, however with a lot bigger normal errors. The constraint (b_{r,j} = b_r rho^j) is not unhealthy. However it will possibly simply go mistaken. For those who do not impose that dividends and value are cointegrated, or with vector aside from 1 -1, in case you permit a small pattern to estimate (rho>1), in case you do not put in dividend yields in any respect and simply lots of short-run forecasters, it will possibly all go badly.

Forecasting bond returns was for me a superb counterexample. A VAR forecasting one-year bond returns from at this time’s yields provides very completely different outcomes from taking a month-to-month VAR, even with a number of lags, and utilizing (A^{12}) to deduce the one-year return forecast. Small pricing errors or microstructure dominate the month-to-month information, which produces junk when raised to the twelfth energy. (Local weather regressions are having enjoyable with the identical situation. Small estimated results of temperature on development, raised to the one hundredth energy, can produce properly calamitous outcomes. However use primary concept to consider items.)

Nakamura and Steinsson (appendix) present how delicate some normal estimates of impulse response capabilities are to those questions.

Weak proof

For the present coverage query, I hope you get a way of how weak the proof is for the “normal view” that increased rates of interest reliably decrease inflation, although with an extended and variable lag, and the Fed has a great deal of management over inflation.

Sure, many estimates look the identical, however there’s a fairly sturdy prior stepping into to that. Most individuals do not publish papers that do not conform to one thing like the usual view. Look how lengthy it took from Sims (1980) to Christiano Eichenbaum and Evans (1999) to supply a response operate that does conform to the usual view, what Friedman informed us to anticipate in (1968). That took lots of taking part in with completely different orthogonalization, variable inclusion, and different specification assumptions. This isn’t criticism: when you will have a robust prior, it is sensible to see if the information will be squeezed in to the prior. As soon as authors like Ramey and Nakamura and Steinsson began to look with a important eye, it grew to become clearer simply how weak the proof is.

Normal errors are additionally broad, however the variability in outcomes resulting from modifications in pattern and specification are a lot bigger than formal normal errors. That is why I do not stress that statistical side. You play with 100 fashions, attempt one variable after one other to tamp down the worth puzzle, after which compute normal errors as if the one hundredth mannequin had been written in stone. This put up is already too lengthy, however displaying how outcomes change with completely different specs would have been a superb addition.

For instance, listed here are a couple of extra Ramey plots of inflation responses, replicating varied earlier estimates

Take your decide.

What ought to we do as a substitute?

Nicely, how else ought to we measure the results of financial coverage? One pure method turns to the evaluation of historic episodes and modifications in regime, with particular fashions in thoughts.

Romer and Romer move on ideas on this method:

…some macroeconomic habits could also be basically episodic in nature. Monetary crises, recessions, disinflations, are all occasions that appear to play out in an identifiable sample. There could also be lengthy intervals the place issues are principally high-quality, which are then interrupted by brief intervals when they don’t seem to be. If that is true, one of the best ways to grasp them could also be to deal with episodes—not a cross-section proxy or a tiny sub-period. As well as, it’s precious to know when the episodes had been and what occurred throughout them. And, the identification and understanding of episodes might require utilizing sources aside from standard information.

A whole lot of my and others’ fiscal concept writing has taken an identical view. The lengthy quiet zero certain is a check of theories: old-Keynesian fashions predict a delation spiral, new-Keynesian fashions predicts sunspot volatility, fiscal concept is according to secure quiet inflation. The emergence of inflation in 2021 and its easing regardless of rates of interest beneath inflation likewise validates fiscal vs. normal theories. The fiscal implications of abandoning the gold normal in 1933 plus Roosevelt’s “emergency” finances make sense of that episode. The brand new-Keynesian response parameter (phi_pi) in (i_t – phi_pi pi_t), which ends up in unstable dynamics for ](phi_pi>1) is just not recognized by time collection information. So use “different sources,” like plain statements on the Fed web site about how they react to inflation. I already cited Clarida Galí and Gertler, for measuring the rule not the response to the shock, and explaining the implications of that rule for his or her mannequin.

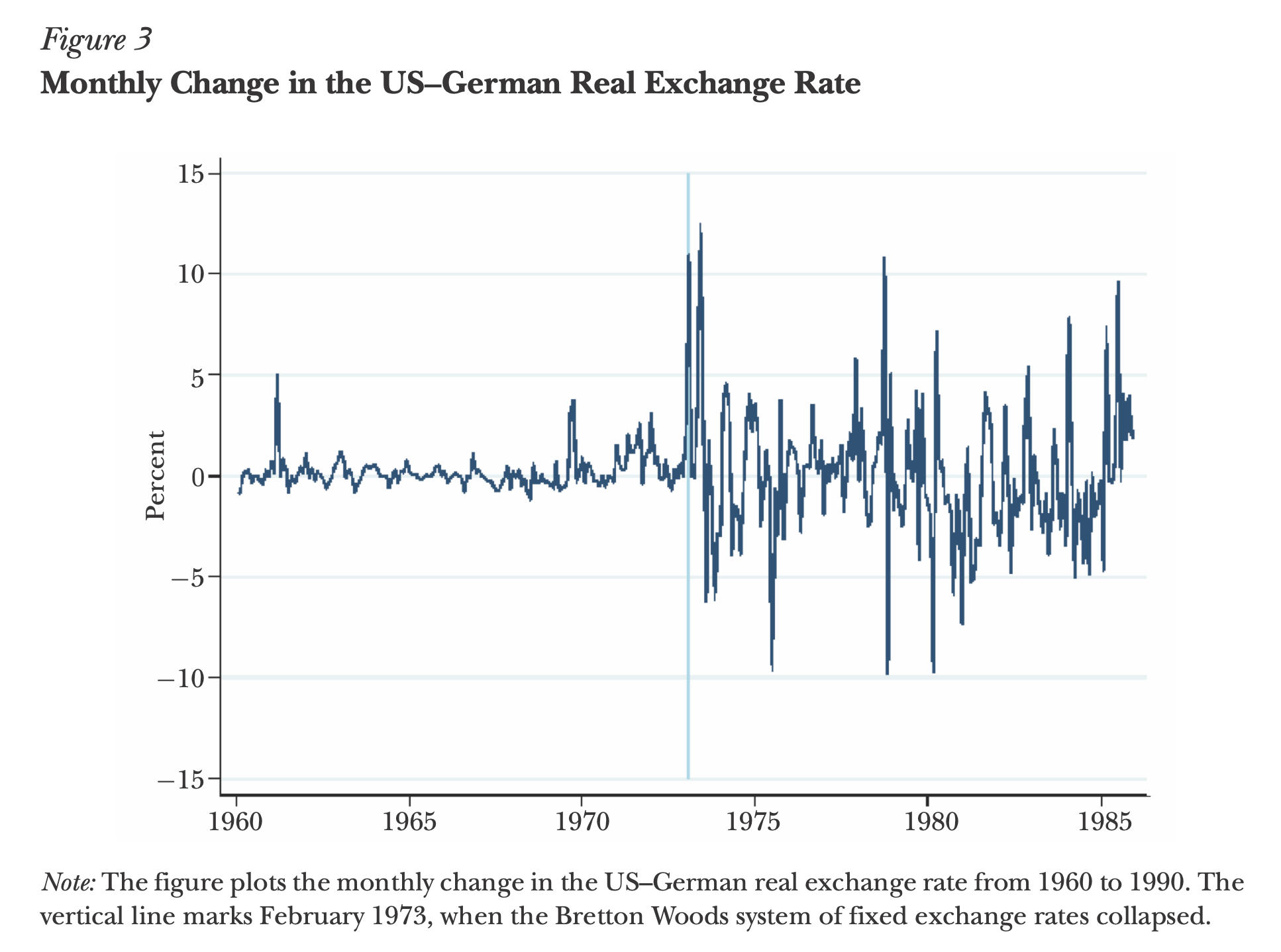

Nakamura and Steinsson likewise summarize Mussa’s (1986) traditional examine of what occurs when international locations change from mounted to floating trade charges:

“The change from a hard and fast to a versatile trade fee is a purely financial motion. In a world the place financial coverage has no actual results, such a coverage change wouldn’t have an effect on actual variables like the true trade fee. Determine 3 demonstrates dramatically that the world we reside in is just not such a world.”

Additionally, evaluation of explicit historic episodes is enlightening. However every episode has different issues happening and so invitations various explanations. 90 years later, we’re nonetheless combating about what induced the Nice Despair. 1980 is the poster little one for financial disinflation, but as Nakamura and Steinsson write,

Many economists discover the narrative account above and the accompanying proof about output to be compelling proof of enormous financial nonneutrality. Nevertheless, there are different doable explanations for these actions in output. There have been oil shocks each in September 1979 and in February 1981…. Credit score controls had been instituted between March and July of 1980. Anticipation results related to the phased-in tax cuts of the Reagan administration can also have performed a task within the 1981–1982 recession ….

Learning modifications in regime, akin to mounted to floating or the zero certain period, assist considerably relative to finding out a selected episode, in that they’ve a few of the averaging of different shocks.

However the attraction of VARs will stay. None of those produces what VARs appeared to supply, a theory-free qualitative estimate of the results of financial coverage. Many inform you that costs are sticky, however not how costs are sticky. Are they old-Keynesian backward trying sticky or new-Keynesian rational expectations sticky? What’s the dynamic response of relative inflation to a change in a pegged trade fee? What’s the dynamic response of actual relative costs to productiveness shocks? Observations akin to Mussa’s graph may help to calibrate fashions, however doesn’t reply these questions instantly. My observations concerning the zero certain or the current inflation equally appear (to me) decisive about one class of mannequin vs. one other, at the least topic to Occam’s razor about epicycles, however likewise don’t present a theory-free impulse response operate. Nakamura and Steinsson write at size about different approaches; model-based second matching and use of micro information specifically. This put up is happening too lengthy; learn their paper.

In fact, as we now have seen, VARs solely appear to supply a model-free quantitative measurement of “the results of financial coverage,” but it surely’s laborious to surrender on the looks of such a solution. VARs and impulse responses additionally stay very helpful methods of summarizing the correlations and cross correlations of information, even with out trigger and impact interpretation.

In the long run, many concepts are profitable in economics after they inform researchers what to do, after they supply a comparatively clear recipe for writing papers. “Have a look at episodes and suppose laborious is just not such recipe.” “Run a VAR is.” So, as you concentrate on how we will consider financial coverage, take into consideration a greater recipe in addition to a superb reply.

(Keep tuned. This put up is prone to be up to date a couple of occasions!)

VAR technical appendix

Technically, working VARs may be very simple, at the least till you begin making an attempt to clean out responses with Bayesian and different strategies. Line up the information in a vector, i.e. (x_t = [i_t pi_t y_t]’). Then run a regression of every variable on lags of the others, [x_t = Ax_{t-1} + u_t]. In order for you multiple lag of the suitable hand variables, simply make an even bigger (x) vector, (x_t = [i_t pi_t y_t i_{t-1} pi_{t-1} y_{t-1}]’).

The residuals of such regressions (u_t) might be correlated, so it’s important to determine whether or not, say, the correlation between rate of interest and inflation shocks means the Fed responds within the interval to inflation, or inflation responds inside the interval to rates of interest, or some mixture of the 2. That is the “identification” assumption situation. You possibly can write it as a matrix (C) in order that (u_t = C varepsilon_t) and cov((varepsilon_t varepsilon_t’)=I) or you may embody some contemporaneous values into the suitable hand sides.

Now, with (x_t = Ax_{t-1} + Cvarepsilon_t), you begin with (x_0=0), select one collection to shock, e.g. (varepsilon_{i,1}=1) leaving the others alone, and simply simulate ahead. The ensuing path of the opposite variables is the above plot, the “impulse response operate.” Alternatively you may run a regression (x_t = sum_{j=0}^infty theta_j varepsilon_{t-j}) and the (theta_j) are (completely different, in pattern) estimates of the identical factor. That is “native projection”. For the reason that proper hand variables are all orthogonal, you may run single or a number of regressions. (See right here for equations.) Both method, you will have discovered the transferring common illustration, (x_t = theta(L)varepsilon_t), within the first case with (theta(L)=(I-AL)^{-1}C) within the second case instantly. For the reason that proper hand variables are all orthogonal, the variance of the collection is the sum of its loading on all the shocks, (cov(x_t) = sum_{j=0}^infty theta_j theta_j’). This “forecast error variance decomposition” is behind my assertion that small quantities of inflation variance are resulting from financial coverage shocks somewhat than shocks to different variables, and principally inflation shocks.

* Some Papers:

[ad_2]